Financing a diamond engagement ring is a smart, and very common, way to manage one of life's biggest and most exciting purchases. It lets you get the perfect ring without having to drain your savings, breaking down a major expense into much more manageable monthly payments. It’s all about making your dream ring a reality today, not someday.

Why Financing Your Diamond Ring Makes Sense

Deciding to buy an engagement ring is a huge milestone. It’s a moment that blends deep emotional meaning with a serious financial commitment. For many couples, buying the ring is one of the very first big financial steps they take together, and it's a key part of financial planning for major life events including marriage.

Let’s be real: paying for the ring all at once isn't practical for most people. That's exactly why exploring diamond engagement rings financing has become the go-to path for so many.

This isn't just about being able to afford the ring—it's about smart money management. When you spread the cost over time, you protect your cash flow and keep your emergency fund safe, all while celebrating your love with a beautiful, lasting symbol. Financing can also open up your options, letting you explore a wider range of diamonds and settings, which our guide to buying engagement rings dives into.

Financing Options at a Glance

Navigating financing can feel a little overwhelming, but it really boils down to just a few key methods. Each one comes with its own terms and is better suited for different financial situations. Having a clear overview helps you quickly figure out which path makes the most sense for your budget and credit profile. This table gives you a quick comparison of the most common ways people finance a diamond ring.

| Financing Method | Typical APR Range | Best For | Key Consideration |

|---|---|---|---|

| Jeweler Financing | 0% - 25%+ | Buyers looking for convenience and special 0% APR offers directly from the store. | Watch out for deferred interest—if you don't pay it off in time, you could be hit with high retroactive interest. |

| Personal Loan | 6% - 36% | People who want a fixed interest rate and predictable monthly payments from a bank. | You'll need a good credit score to get the best rates, and it can take longer to get approved. |

| Credit Card | 0% Intro / 18% - 29% | Anyone with a card offering a 0% introductory APR on new purchases. | Standard interest rates are high once the promotional period ends. |

| Buy Now, Pay Later | 0% - 30% | Shoppers who prefer simple, short-term installment plans for smaller amounts. | Payment plans are often short (like 4 payments over 6 weeks), which can mean higher individual payments. |

Ultimately, choosing the right financing plan helps you buy with confidence. The goal is to find a path that fits comfortably within your budget while letting you get the ring that truly tells your story.

The U.S. engagement ring market is massive, on track to hit $12.5 billion in 2025. With the average ring costing around $5,800, it’s easy to see why nearly 60% of buyers choose a payment plan to manage the cost without wiping out their savings.

Translating the Fine Print of Ring Financing

Before you sign on the dotted line, you need to speak the lender's language. Think of any financing offer like a recipe—each component changes the final result. Getting comfortable with these terms means you know exactly what you’re signing up for, putting you in control of what that diamond engagement ring really costs.

It’s not about doing complicated math in your head. It’s simply about understanding how a few key numbers can dramatically shift what you’ll pay over time.

The Core Ingredients of Your Financing Plan

Every loan or financing plan is built on four pillars. Each one plays a critical role in shaping both your monthly payment and the total cost.

- Principal: This is your starting point—the total amount you borrow to buy the ring. If the ring is $7,000 and you put some cash down, the leftover amount is your principal.

- Down Payment: This is the cash you pay upfront. A bigger down payment shrinks your principal, which means you borrow less and almost always pay less interest over the life of the loan.

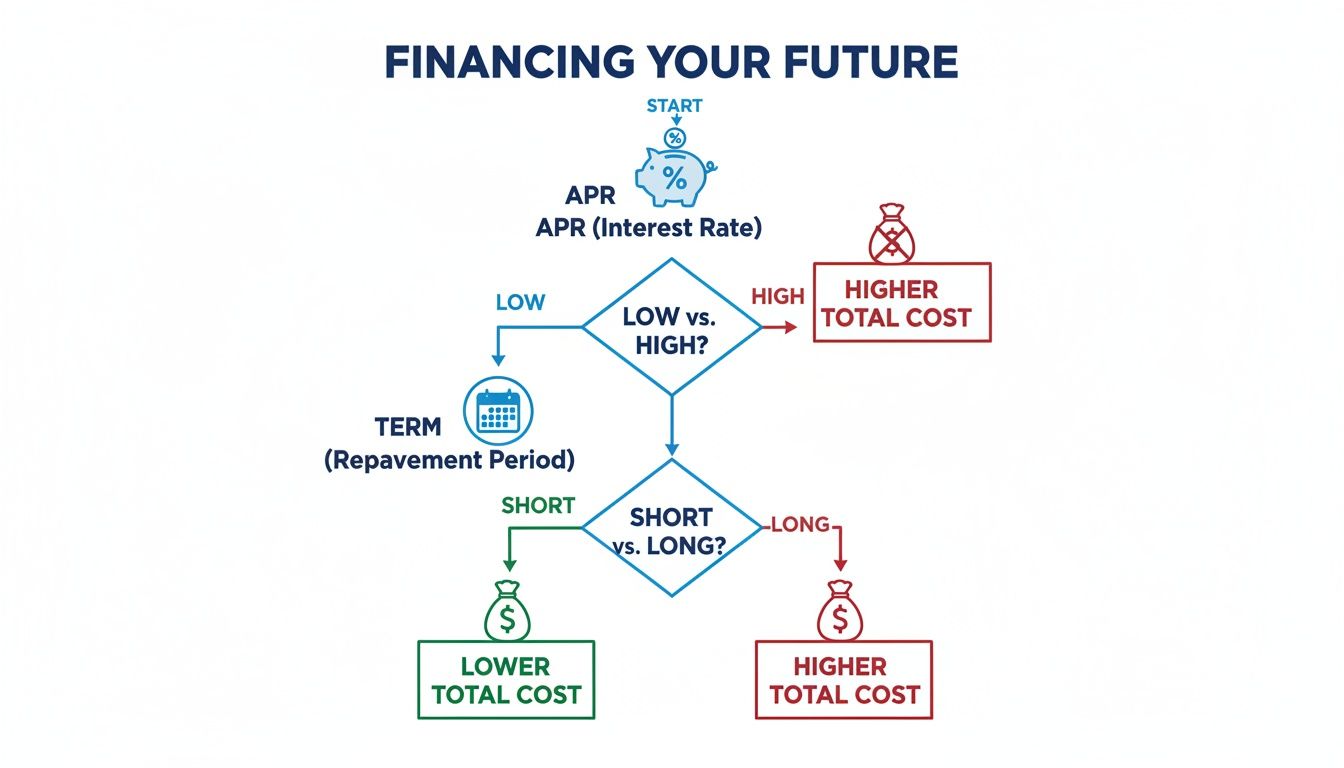

- APR (Annual Percentage Rate): Think of APR as the "rental fee" on the money you borrow, shown as a yearly percentage. It bundles the interest rate and other fees, making it the truest measure of a loan's cost. A lower APR always means a cheaper loan.

- Term: This is the loan's lifespan—how long you have to pay it back, usually shown in months (like 24, 36, or 60 months). A shorter term means higher monthly payments but less total interest. A longer term drops your monthly payment but racks up more interest in the end.

These four elements work together, determining not just your monthly bill but the ring's true final price tag.

How APR and Term Change Everything

Let's see this in action. Imagine you're financing a $6,000 engagement ring with zero money down. The only things we'll change are the APR and the term.

Scenario A: The Short-Term, Low-Interest Plan

- APR: 7%

- Term: 24 months (2 years)

- Monthly Payment: Approximately $268

- Total Interest Paid: $442

- Total Cost of Ring: $6,442

This is a fantastic option if you can handle the higher monthly payment. You'll own the ring free and clear in just two years and save a ton on interest.

Scenario B: The Long-Term, Higher-Interest Plan

- APR: 15%

- Term: 60 months (5 years)

- Monthly Payment: Approximately $143

- Total Interest Paid: $2,559

- Total Cost of Ring: $8,559

That low monthly payment looks tempting, doesn't it? But the higher APR and five-year term mean you'll pay over $2,100 more in interest than in Scenario A.

Understanding these trade-offs is crucial. A lower monthly payment can be tempting, but it often masks a much higher total cost. Always calculate the full price before committing to any diamond engagement rings financing plan.

Sometimes, financing gets tricky, especially if your credit history isn't perfect. In those cases, you may need to explore other paths. For a deeper look into those alternatives, you might be interested in learning about no credit check jewelry financing and how it works. By decoding the fine print of every offer, you can confidently choose the financing that aligns with your budget and lets you celebrate your love without any future regrets.

Comparing Your Best Financing Paths

Choosing how you'll pay for the ring is just as critical as picking the perfect diamond. Every financing option comes with its own mix of convenience, cost, and fine print. Getting familiar with the landscape—from a quick approval at the jewelry counter to a structured personal loan—is the key to finding a plan that fits your budget without adding stress.

Let's walk through the most common ways to finance an engagement ring.

This chart breaks down how the two biggest factors in any loan, the APR and the term length, directly affect what you'll ultimately pay.

Remember, a lower monthly payment isn't always the best deal. Stretching out the loan can mean you pay a lot more in total interest over time.

In-Store Jeweler Financing

This is usually the path of least resistance. Jewelers, including us right here at ECI, often partner with lenders to offer financing on the spot. The main attraction is almost always a promotional 0% APR offer.

These deals are perfect if you can clear the balance within the promotional period, which typically runs from 6 to 24 months. But there's a huge catch you need to know about: deferred interest. If you have even a single dollar left to pay when that promo ends, you'll get hit with all the interest that's been quietly adding up from day one, often at a steep rate of 25% or more.

- Best For: Disciplined buyers with a solid credit score (think 670+) who are completely confident they can pay off the ring before the 0% APR deal expires.

- Credit Score Needed: Typically good to excellent.

- Application Process: Super fast. It's often done in the store or online in minutes. We've made our own ECI Jewelers financing options as seamless as possible.

Personal Loans

A personal loan from a bank, credit union, or online lender gives you a lump sum of cash that you pay back in fixed monthly installments. The biggest advantage here is predictability. Your interest rate is locked in, so your payments never change, making it incredibly easy to budget.

When you're shopping around, personal loans from lenders like Sofi can offer competitive rates. The application is a bit more involved than in-store options—they'll want to see proof of income and do a full credit check. However, the interest rates are almost always much lower than a standard credit card, especially if you have a strong credit history.

- Best For: Anyone who values predictable, fixed payments and wants to steer clear of deferred interest traps. It’s a great, stable choice for larger purchases you plan to pay off over a few years.

- Credit Score Needed: Good to excellent (670+) will get you the best rates, but some lenders will work with fair credit.

- Application Process: This can take a few days. Be prepared with documents like recent pay stubs and bank statements.

Think of a personal loan as taking a well-marked trail up a mountain. The path is clear, you know exactly how long the hike will be, and there are no hidden surprises. In-store financing, on the other hand, can feel like a shortcut that turns into a much longer journey if you miss a single step.

Credit Cards

Using plastic is another go-to, especially if you have a card with a 0% introductory APR on new purchases. It works a lot like store financing, giving you a window of time to pay off the ring interest-free. The main difference is that your credit line isn't tied to one specific jeweler.

But just like with store financing, once that intro period is over, the regular purchase APR applies, which can be pretty high (18% to 29%). This route requires the same discipline: you have to pay the balance in full before the clock runs out. On the plus side, it's an excellent way to rack up rewards points or cash back on a big-ticket item.

- Best For: People who already have a credit card with a great 0% intro offer and have a solid plan to pay it off within that timeframe.

- Credit Score Needed: Good to excellent (670+) is usually required to qualify for the premium cards that offer these promotional rates.

- Application Process: If you already have the card, it's instant. If you're applying for a new one, approval can take anywhere from a few minutes to a few days.

Buy Now Pay Later Services

Services like Affirm, Klarna, and Afterpay are popping up everywhere, and jewelry is no exception. They let you split the cost of the ring into a handful of fixed payments. For smaller amounts, it's often four installments over six weeks, but for big purchases like a ring, they offer longer-term monthly plans.

Many of these BNPL plans come with 0% APR, which makes them a tempting short-term fix. The application is incredibly simple and usually only requires a soft credit check, so it won't ding your credit score. With the average U.S. engagement ring now costing around $5,800, it’s no surprise so many couples are turning to these services. It also fits a broader trend where 71% of young couples are looking for more sustainable and budget-friendly choices, often pairing flexible payments with beautiful lab-grown diamonds.

- Best For: Buyers who want a simple, transparent, short-term payment plan without a hard credit inquiry.

- Credit Score Needed: It varies, but they are often more accessible to people with fair or limited credit history.

- Application Process: Usually happens right at checkout online and approval is almost instant.

How Your Credit Score Shapes Your Options

When you apply for financing for a diamond engagement ring, your credit score is the single most important number a lender looks at. Think of it as your financial resume—it’s a quick snapshot that tells lenders how reliably you’ve managed money and debt in the past.

A strong score signals low risk, which means lenders are eager to offer you their best deals. You’ll unlock lower interest rates and more flexible payment terms. A lower score, on the other hand, suggests higher risk, leading to higher interest rates to protect the lender. This number directly impacts your monthly payment and how much you'll pay for the ring over its lifetime.

How Lenders See Your Score

Lenders group scores into tiers. While the exact numbers might differ slightly from one place to the next, the structure is pretty consistent. Knowing where you stand helps you set realistic expectations for the kind of offers you'll receive.

- Excellent Credit (740+): You're the ideal applicant. Lenders will roll out the red carpet for you with their best offers, including 0% APR promotions and the absolute lowest rates on personal loans.

- Good Credit (670-739): You’re still seen as a very reliable borrower. You’ll have no trouble qualifying for most financing options, but your interest rates might be a touch higher than someone in the excellent tier.

- Fair Credit (580-669): This is where your options start to narrow and get more expensive. You likely won't qualify for those tempting 0% APR deals, and any loan you get will come with a significantly higher interest rate.

Let's see just how much this can affect the total cost of the exact same ring.

The True Cost of a $6,000 Ring Across Different Credit Scores

Imagine three different people are buying the same beautiful $6,000 diamond ring. They all choose a 36-month (3-year) personal loan. The only thing separating them is their credit score. This simple comparison shows how much a good score can save you.

| Credit Score Tier | Typical APR | Monthly Payment | Total Interest Paid | Total Ring Cost |

|---|---|---|---|---|

| Excellent (740+) | 7% | $185 | $660 | $6,660 |

| Good (670-739) | 14% | $205 | $1,380 | $7,380 |

| Fair (580-669) | 22% | $229 | $2,244 | $8,244 |

Look at that difference. The person with fair credit ends up paying $1,584 more than the person with excellent credit—for the very same ring. That’s a huge chunk of change that could have gone toward the wedding, a honeymoon, or into your savings account.

Your credit score isn't just a number; it's a powerful tool for saving money. Improving it by even a few points can put hundreds, or even thousands, of dollars back into your pocket when financing an engagement ring.

Quick Ways to Strengthen Your Score Before You Apply

The great news is that you can take action right now to give your score a boost before you even start ring shopping. A little effort upfront can put you in a much stronger position.

- Check Your Credit Reports for Errors: Pull your free reports from the big three bureaus: Equifax, Experian, and TransUnion. Go through them line by line. If you spot a mistake, like an account that isn't yours or a late payment you know you made on time, dispute it immediately.

- Pay Down Your Credit Card Balances: Lenders pay close attention to your credit utilization ratio—how much of your available credit you're using. A high ratio is a red flag. Aim to get all your card balances below 30% of their limits. This one move can give your score a quick, meaningful boost.

- Ensure On-Time Payments: Your payment history is the biggest piece of the credit score puzzle. If you have any accounts that are past due, get them current right away. Then, set up automatic payments to make sure you never miss a due date again.

Taking these simple steps helps you secure the best possible financing for a diamond engagement ring. It's a proactive approach that saves you money and reduces stress, letting you focus on what really matters—the proposal.

A Practical Checklist for Securing Your Financing

Figuring out diamond engagement ring financing can feel like a maze, but a solid game plan makes it a surprisingly simple process. This checklist breaks everything down into easy, manageable steps so you can go from just looking to confidently buying.

Think of it as a roadmap. Following it helps you sidestep the common mistakes and lock in the best possible terms for the ring. The key is to handle your financing strategically from the start, not as a last-minute scramble.

Step 1: Lay the Financial Groundwork

Before you start dreaming about carat sizes and settings, you need a clear picture of your own finances. Honestly, this prep work is the most important part of the entire journey. It’ll save you a ton of stress down the road.

- Set a Realistic Budget: Take a hard look at your monthly income and expenses. Figure out a payment you can actually afford without feeling squeezed. Don't fixate on the ring's total price tag; focus on what fits comfortably into your life right now.

- Check Your Credit Score: Your credit score is what gets you in the door for the best financing deals. Use a free service to pull your score so you know exactly where you stand. If it’s not where you want it to be, it’s worth taking a few months to improve it before you apply for anything.

- Gather Your Documents: Lenders will want to see proof of income (like recent pay stubs), proof of address (a utility bill works great), and a government-issued ID. Having these ready to go makes the application process way faster and smoother.

Step 2: Compare Your Financing Options

Whatever you do, don't just jump on the first offer you see. Shopping around for financing is just as critical as shopping for the ring itself. Getting a few pre-approvals gives you serious leverage and a clear head.

Start by asking for a pre-approval from your personal bank or credit union. Then, check out some online personal loan providers and maybe even look into a credit card with a 0% APR introductory offer. When you compare these real, concrete offers side-by-side, you'll see the true cost of each one. It makes picking the option with the lowest interest and best terms a no-brainer.

The market for diamond engagement rings is booming, expected to jump from $32.37 billion in 2024 to nearly $43.98 billion by 2031, and accessible financing is a huge reason why. These payment plans are especially popular with millennials, where 70% are drawn to interest-free periods that help them manage a big purchase without disrupting their other financial goals. You can find more on the growing diamond ring market on datainsightsmarket.com.

Step 3: Finalize the Purchase with Confidence

Okay, you’ve got your financing lined up and your budget locked in. Now for the fun part. But even here, being strategic really pays off.

- Negotiate the Ring Price First: Always, always agree on the final price of the ring before you even bring up how you’re paying. Mentioning financing too early can sometimes make a jeweler less willing to be flexible on the price.

- Read Every Word of the Agreement: This is non-negotiable, especially for those tempting 0% APR deals. You need to understand the deferred interest clause—know the exact date the promo period ends and what that scary penalty APR will be if you haven't paid it off in time.

- Set Up Automatic Payments: The moment the purchase is done, go into your bank app and set up automatic payments. It’s the single best way to guarantee you never miss a due date, which protects your credit score and helps you avoid nasty late fees or penalty interest.

Your Top Ring Financing Questions, Answered

Let's be honest, figuring out the financing for a diamond engagement ring can feel a little overwhelming. It's a huge purchase, and you want to get it right. We get these questions all the time from couples just like you, so let's clear up any confusion.

Here are the direct, practical answers to the most common concerns we hear.

Is It a Bad Idea to Finance an Engagement Ring?

Financing a ring isn't good or bad on its own—it's just a financial tool. How you use it is what matters.

It's a brilliant idea if you lock in a low or 0% interest rate and have a rock-solid plan to pay it off before the promotional period ends. This strategy lets you get the perfect ring without wiping out your savings, which is always a smart move.

On the flip side, it becomes a bad idea if you get stuck with a high-interest plan, the monthly payments are a stretch, or you get blindsided by the "deferred interest" trap on a 0% APR deal.

Think of it like any other major loan. Budget for it, read every single line of the agreement, and make sure the payments fit comfortably into your life. When you do that, financing is an incredibly helpful option.

Can I Finance an Engagement Ring with Bad Credit?

Yes, you can, but your options will be fewer and much more expensive. Big banks and prime credit card issuers will likely turn you down, so you'll need to look at other avenues.

You'll probably have better luck with jewelers offering in-house financing programs that are designed for a wider range of credit scores. Lenders who specialize in subprime personal loans are another route.

Just be prepared for much higher APRs in these situations. This will significantly increase the total amount you pay for the ring over time. Lease-to-own programs are also out there, but they almost always end up being the costliest choice. The best financial strategy, if you can, is to spend a few months boosting your credit score before you start shopping.

Does Applying for Ring Financing Hurt My Credit Score?

When you submit a formal application for a credit card, loan, or store financing, the lender does what's called a "hard inquiry" on your credit report.

A single hard inquiry usually just causes a small, temporary dip in your score—typically less than five points. It’s not a big deal. However, applying for several different lines of credit in a short period can have a more noticeable negative impact.

The best way to avoid this is to look for lenders who offer a "pre-qualification" process first. This uses a "soft inquiry," which doesn't affect your credit score at all. Getting pre-qualified with a few different options lets you compare real rates before you have to commit to an official application and the hard inquiry that comes with it.

What Happens if I Miss a Payment on a 0% APR Plan?

Missing a payment on a promotional 0% APR plan is a mistake you really want to avoid. The consequences can be serious and very expensive.

First, you'll almost definitely get hit with a late fee right away.

More importantly, you'll probably lose your 0% interest rate. Most of these deals have a "deferred interest" clause hidden in the fine print. This means if you miss a payment or don't pay off the entire balance by the deadline, the lender can charge you all the interest that's been quietly adding up since the day you bought the ring. This is often at a sky-high penalty APR of 25-30%.

That one slip-up can instantly add hundreds, or even thousands, of dollars to what you owe, turning a great deal into a huge financial headache.

At ECI Jewelers, we believe finding the perfect ring should be one of the happiest moments of your life, not a source of stress. We offer clear, flexible financing options to help you celebrate your love with total confidence. Explore our stunning collection of diamond engagement rings and discover a payment plan that works for you.

{kind=link}